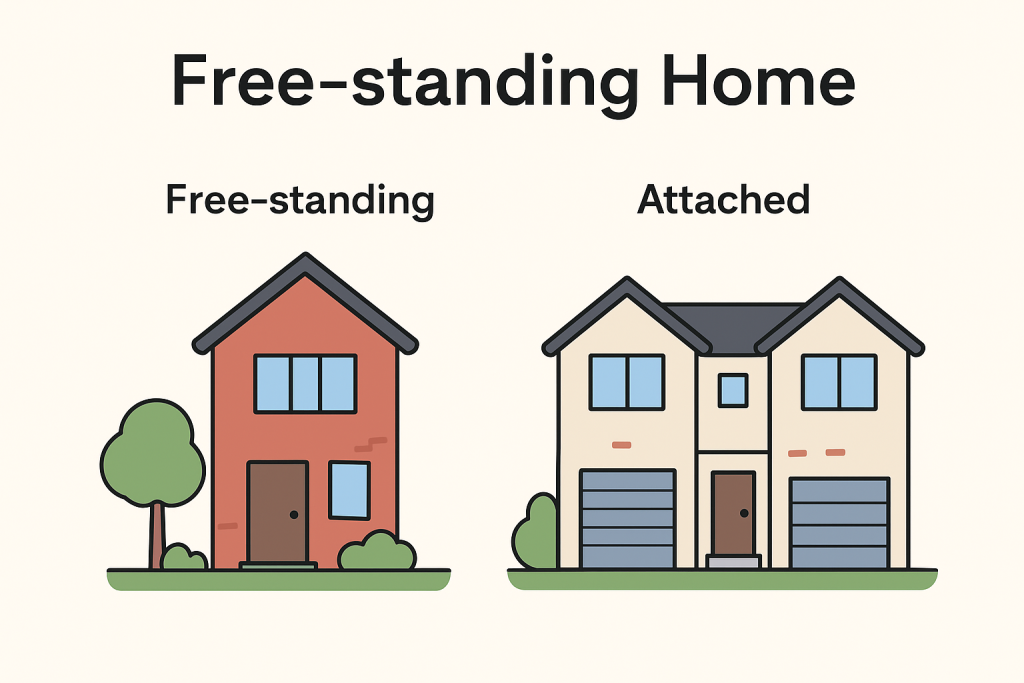

In Australia, a free-standing home (also called a detached house) is a standalone residential building that sits on its own block of land and doesn’t share any walls with neighbouring houses.

Free-standing Home (Detached House)

A free-standing home is a single, independent dwelling that:

- Is not attached to any other home or structure

- Has its own private yard or garden space

- Is built on a separate title or land lot

Key Features

Key Features

- Complete privacy — no shared walls

- Typically larger land area

- You’re responsible for all maintenance (house + garden)

- Usually includes a driveway, backyard, and garage

- Offers flexibility for extensions, renovations, or a granny flat

Ownership

You own both:

- The building, and

- The land it sits on

No body corporate or strata fees apply (unlike apartments or townhouses).

Example

If you buy a free-standing home in Sydney or Melbourne suburbs, you’ll have:

- A detached house on its own land

- Possibly a front and back yard

- Full control over how you maintain or modify your property

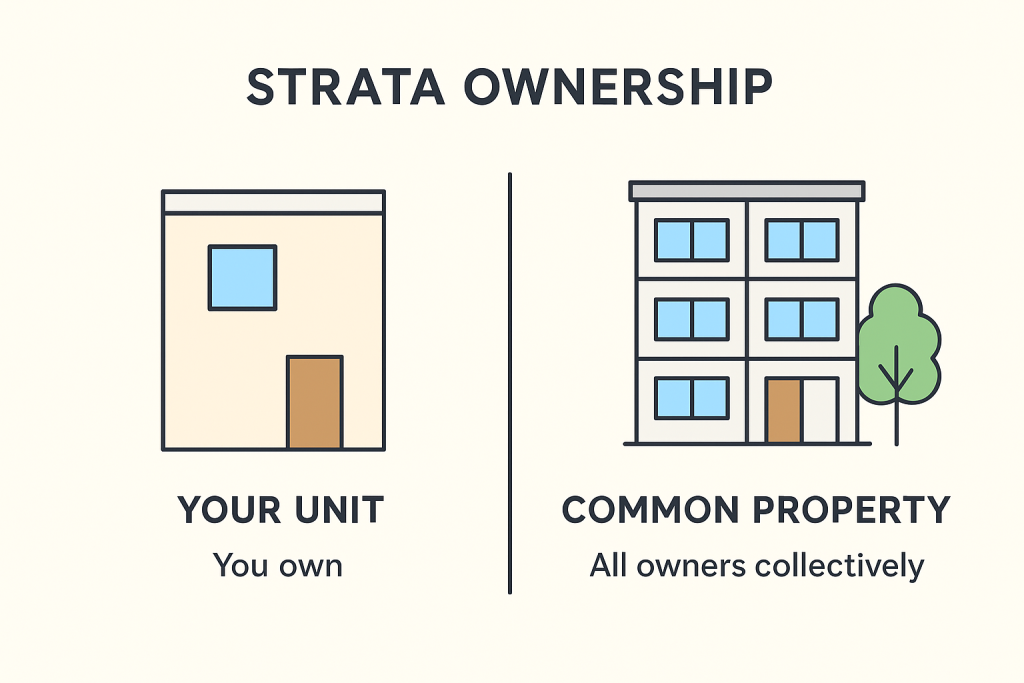

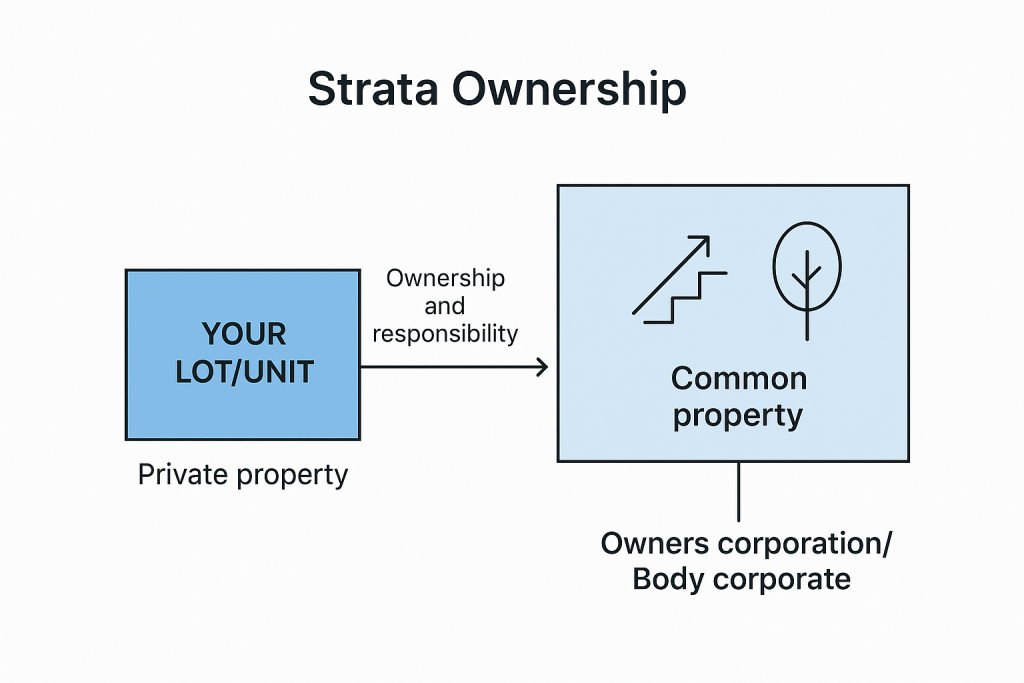

In Australia, strata refer to a form of property ownership and management used for buildings or complexes that have multiple units or lots, such as apartments, townhouses, or villas.

What “Strata” Means

When a property is under strata title, it means:

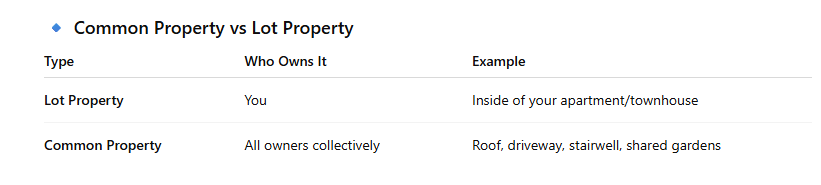

- You own your individual unit or lot (for example, your apartment or townhouse), and

- You share ownership and responsibility for the common areas of the property.

Common Areas Include:

- Hallways, lifts, gardens, and driveways

- Roofs, walls, and external structures

- Shared facilities like pools, gyms, or parking

Who Manages It

- A body corporate (also called an owners corporation) manages the property.

- All owners automatically become members of this group.

- They collect strata fees to cover maintenance, insurance, and repairs.

Example

If you own an apartment:

- You own the inside of your unit.

- The building exterior, foyer, car park, and garden are shared with other owners.

You pay strata levies for upkeep and repairs of these shared spaces

In Australia, home insurance is a policy that protects your house and belongings from damage, loss, or theft. It gives you financial protection if something unexpected happens — like a fire, storm, flood, or burglary.

Types of Home Insurance

- Building Insurance

- Covers the structure of your home — walls, roof, floors, garage, fences, etc.

- Protects against fire, storm, flood, vandalism, or accidental damage.

- Required by lenders if you have a home loan.

Example: If a storm damages your roof, building insurance pays for repairs.

- Contents Insurance

- Covers your belongings inside the home, like furniture, appliances, jewellery, clothes, and electronics.

- Protects against theft, fire, or accidental damage.

Example: If your TV or laptop is stolen, contents insurance covers the replacement.

Combined Home & Contents Insurance

- Offers both building and contents cover in one policy.

- Common choice for homeowners living in their own property.

- Landlord Insurance

- For rental property owners.

- Covers the building, plus damage caused by tenants, rent loss, and legal expenses.

- Strata Insurance

- Applies to apartments or townhouses under strata title.

- Covers common areas (roof, walls, lifts, etc.) — managed by the body corporate.

Common Events Covered

Fire or explosion Storm, hail, or flood Theft or vandalism Accidental damage Burst pipes or water leaks Temporary accommodation if your home becomes unlivable

Fire or explosion Storm, hail, or flood Theft or vandalism Accidental damage Burst pipes or water leaks Temporary accommodation if your home becomes unlivable

Not Always Covered

- General wear and tear

- Poor maintenance

- Termite or pest damage

- Intentional damage